Higher mortgage stress test also putting the squeeze on renewals

Banks have been hiking mortgage rates for renewals and experts say expect more to come

It's not just new homeowners who are feeling the impact of higher interest rates and tougher lending standards:even those who bought years ago are feeling the heat of increased scrutiny.

In January, new rules brought in a so-called "stress test" for mortgage borrowers, wheretheir finances are tested to make sure they would be able to pay higher rates. The benchmark that must be metis either the average of what the big banks currently offer as their posted rate for a five-year fixed term, or two percentage points higher than the actual loan.

"They want to make sure you can afford your mortgage with a good, solid rate in place," saidCynthia Holmes, with the Faculty of Real Estate Management at Toronto's Ryerson University."Not that you can only afford it if rates are really really low."

If you can't pass the test at a federally regulated lender, the lender isn't allowed to give you the loan,which either forces you into a smaller mortgage and cheaper homeor out of the market entirely.

As a result of the new rules, mortgage brokers say new buyers are seeing their purchasing power drastically reduced. Others are flocking to alternative lenders or credit unions, who are outside the new rules.

But for those coming up for mortgage renewal at one of the big banks, the new rules are making it much harder to leave their existing lenders in many cases forcing them to re-up at higher rates.

That's what happened to Toronto-area homeowner Sharan Mahesan.

"We knew our mortgage was going to be up for renewal in June," Mahesan said of his loan on the Markham home he bought in 2011. "But when we got the notice saying we had to renew, they provided us a rate which was significantly higher than what we were paying previously."

Mortgage brokerVarshan ThavarajahsaysMahesan's experience is common as of late, noting that the big banks he works with have been sending out renewal options anywhere from 20 to 50 basis points or between 0.2 and 0.5 per cent higher than the previous loan's term.

And that's just based on the modest rate hikes that have already happened. The five-year Canadian government bond hit its highest level in more than seven years on Tuesday morning, which raises financing costs for the big banks.They can be expected to soon turn around and pass those added costs on to borrowers.

Financing costs may legitimately be going up,but according to Bank of Canada numbers,some $700 billion of mortgage debt is up for renewal in the next 12 months,which is going to give the big banks ample opportunity to renegotiate loans in this era of new laws and possibly squeeze more money out of their existing customers.

Borrowers don't have to undergo a stress testwhen they renew with their existing lenderonly when they switch.That gives the existing lender a window to offer a higher rate, asthey know the borrower may not bein the bestposition to leave.

Small fees add up

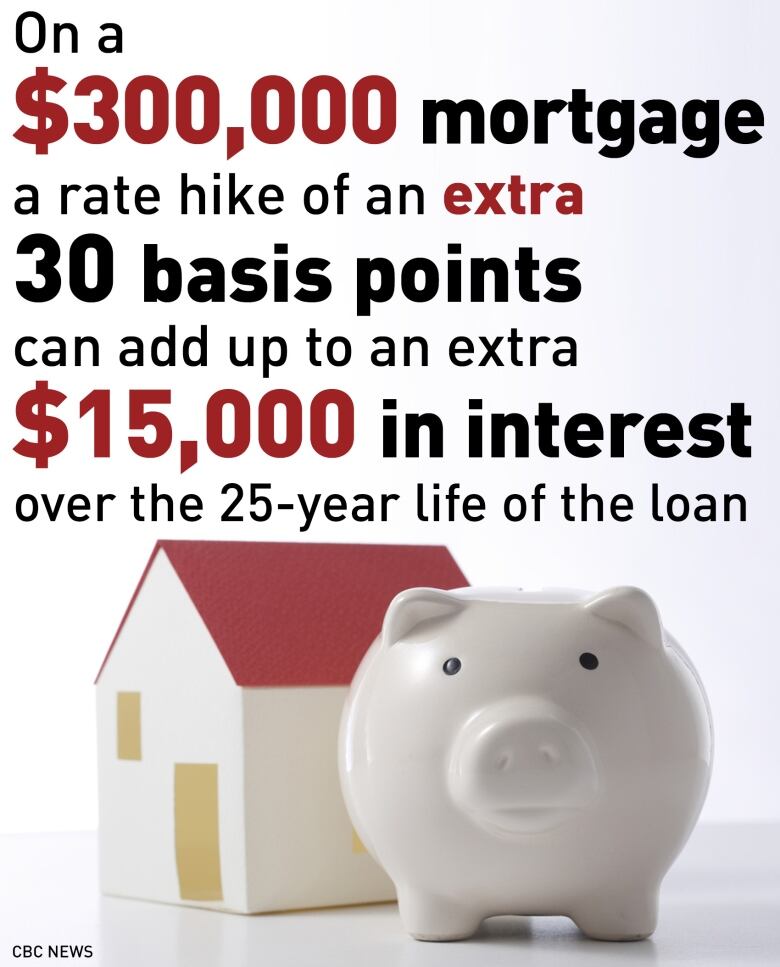

The fees sound small butcan add up. On a $300,000 mortgage, even a tiny rate hike of an extra 30 basis points on a 25-year mortgage at a fixed rate of 3.74 per cent for five yearscan add an extra$15,000 in interest costs over the entire life of theloan. That's an extra $50 per month.On larger mortgages, the increase would be even more.

In Mahesan's case, the rate he was first offered represented several hundred dollars more every mortgage payment. He managed to pass the stress test, sohe was able to negotiate a better rate with his lender. But even then,his new rate is still higher than his old one, and he said he had to go through the paperwork rigmarole of basically applying for a new loan.

"I guess we got spoiled by the rates and the monthly payments," he said.

Thavarajahsaidhe's seen a lot of that sentiment:"There's a lot of shock in our clients'reactions."

Holmes points outthat 86 per cent of borrowers end up renewing their mortgage with their original lendera trend the banks are clearly trying to leverage to their advantage in the stressful new world of stress tests.

Thavarajahsaid whilehe's seen a slowdown in his business from new buyers, he's experienceda surge in the number of people coming to him for advice on the sticker shock while renewing. While most have options, he admits the mortgage landscape has changedand not necessarily in borrowers' favour.

His advice is blunt: "It's important to shop around," he said. "Don't just sign it."

_(720p).jpg)

OFFICIAL HD MUSIC VIDEO.jpg)

.jpg)